Contract labor is no longer a secondary hiring lever. In several U.S. industries, it now absorbs a meaningful share of total labor spend and, in some cases, functions as the default staffing model for critical roles. This shift is not driven by convenience. It reflects structural constraints that permanent hiring cannot resolve.

For contract workers, this creates sustained demand but also sharper competition and tighter scrutiny. For business owners, it forces a recalibration of hiring budgets that once assumed contingent labor would remain marginal.

Why Contract Labor Is Taking a Larger Share of Hiring Budgets

The increase in contract labor spending is not primarily about flexibility. It’s about capacity.

Organizations are facing three overlapping pressures: persistent skill shortages, project-based demand that outpaces internal teams, and wage inflation that makes permanent hiring slower and riskier. Contract labor addresses all three, often at a premium, but with fewer long-term obligations.

In budget terms, this shows up less as incremental spending and more as reallocation. Funds that once supported open requisitions, overtime, or retention bonuses are being redirected toward contingent roles that can be activated quickly and released without severance or restructuring costs.

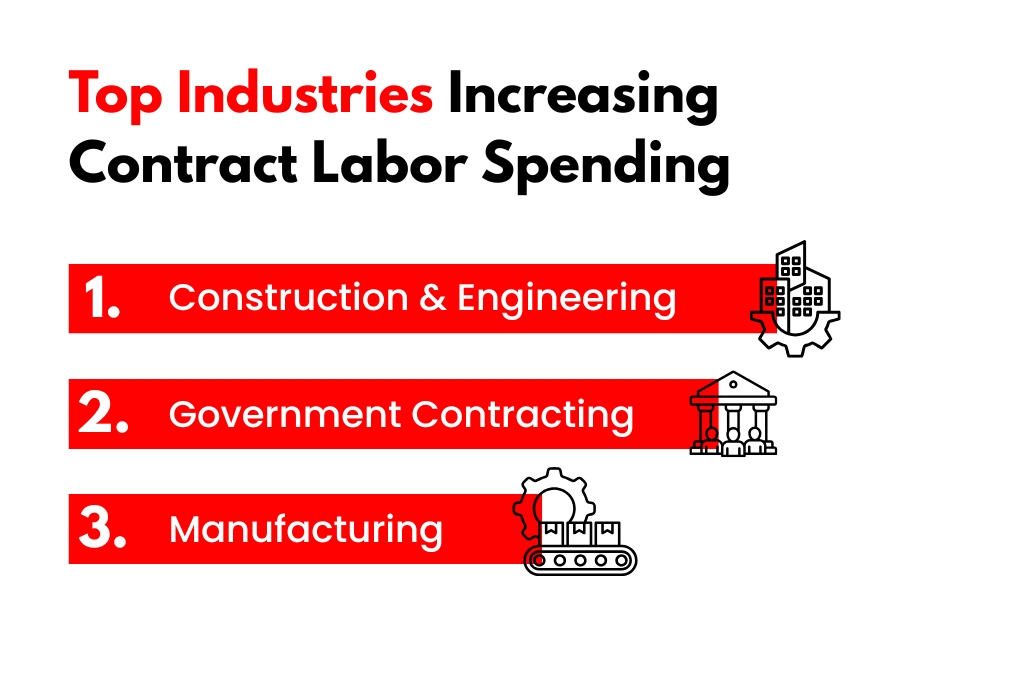

Construction and Engineering: Contract Labor as Project Insurance

Construction and engineering firms are increasing contract labor spending for a different reason. Project pipelines are volatile, and the penalty for under-resourcing a live build is severe.

Data center construction, infrastructure upgrades, and renewable energy projects all require specialized trades and engineers who are difficult to keep fully utilized between projects. Rather than expand permanent headcount, firms are budgeting for contract crews that scale with project phases.

Deloitte’s engineering and construction outlook points to labor availability as one of the sector’s most persistent constraints, particularly for skilled trades tied to complex builds.

Contract workers in this sector are seeing longer engagement cycles than in the past. Multi-year projects increasingly rely on rolling contract renewals rather than short-term placements, blurring the line between contingent and permanent work.

Government Contracting: Stable Spend, Narrower Access

Federal and state agencies remain among the largest buyers of contract labor, particularly in defense, healthcare administration, and IT modernization. Total contract obligations continue to rise as agencies rely on vendors to supply skills that civil service hiring cannot deliver quickly.

Unlike private industry, government contract labor spend is less reactive to economic cycles. Procurement timelines and funding authorizations create a steadier demand profile.

For contractors, this stability comes with tradeoffs. Security clearances, compliance requirements, and vendor consolidation limit access. Rates are often fixed for longer periods, reducing short-term upside but improving predictability.

Manufacturing: Contract Labor Moves onto the Factory Floor

Manufacturing has historically relied less on contract labor for core production roles. That pattern is changing.

Research from the National Bureau of Economic Research shows a long-term increase in the share of contract workers performing production tasks, particularly in facilities with fluctuating output or specialized assembly needs.

Manufacturers are using contract labor to manage demand swings and avoid permanent wage commitments during uncertain cycles. For skilled operators and maintenance specialists, this has opened opportunities beyond traditional temp roles, though job security remains tied to plant utilization.

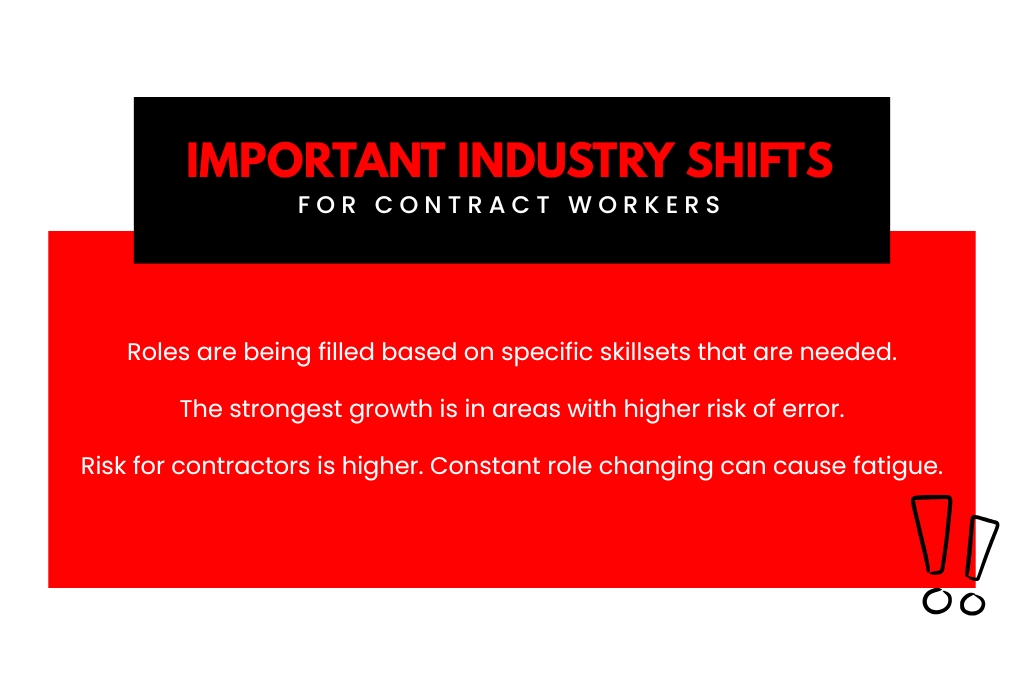

What This Shift Means for Contract Workers

Higher contract labor spend does not automatically translate into better conditions for all contractors.

Demand is concentrating on proven skill sets. Rate growth is strongest where onboarding time is long or errors carry regulatory or safety risk. At the same time, vendor consolidation means fewer entry points into large organizations.

Contractors are also absorbing more risk. Gaps between assignments, benefit costs, and compliance responsibilities increasingly fall on the worker rather than the employer. In sectors like healthcare, frequent role changes can create professional fatigue even as pay remains strong.

What Business Owners Are Learning the Hard Way

Contract labor solves immediate staffing problems but exposes budgeting blind spots.

Organizations that treat contract labor as discretionary often underestimate total cost, especially when premium rates persist longer than planned. Others discover that over-reliance on contractors erodes institutional knowledge and strains permanent teams tasked with coordination and oversight.

More disciplined employers are now tracking contract workforce spend alongside full-time labor metrics, not separately. This allows clearer decisions about when to convert roles, renegotiate vendor terms, or invest in internal capability instead.

Where Contract Labor Spend Is Headed Next

Two patterns are becoming harder to ignore.

First, contract labor is increasingly used to test roles before they exist permanently. In technology and engineering, organizations are using contractors to validate workflows and demand before committing to full-time hiring.

Second, industries with chronic shortages are normalizing higher baseline contract spend rather than attempting to eliminate it. In healthcare and construction, the question is no longer how to reduce contract labor but how to stabilize it.

PeopleSolutions tracks these shifts across industries to help organizations understand where flexibility has become structural rather than temporary.

Conclusion

Contract labor spend in 2026 reflects structural labor constraints, not short-term experimentation. Construction, government, and manufacturing are increasing reliance on the contract workforce because permanent hiring cannot absorb demand fast enough or flexibly enough.

For contract workers, opportunity remains strong but increasingly concentrated. For business owners, the challenge is no longer whether to use contract labor, but how to budget for it without losing control of costs or capability.