Walk into any mid-sized bank during exam prep season and you’ll spot them: the consultants who’ve done this exact audit at four other banks, the AML analyst who knows your transaction monitoring system better than your own staff, the guy who wrote half the policies your examiners are about to review.

They’re expensive. They leave in three months. And you’ll probably hire them again next year.

Contract compliance work has quietly become how banks staff their riskiest projects. Not because it’s cheaper (it isn’t). And not because banks can’t find full-time people, though that’s getting harder. They do it because when the OCC schedules an exam in six weeks, you can’t tell your board you’re still interviewing candidates.

Table of Contents

The Timeline Problem Nobody Talks About

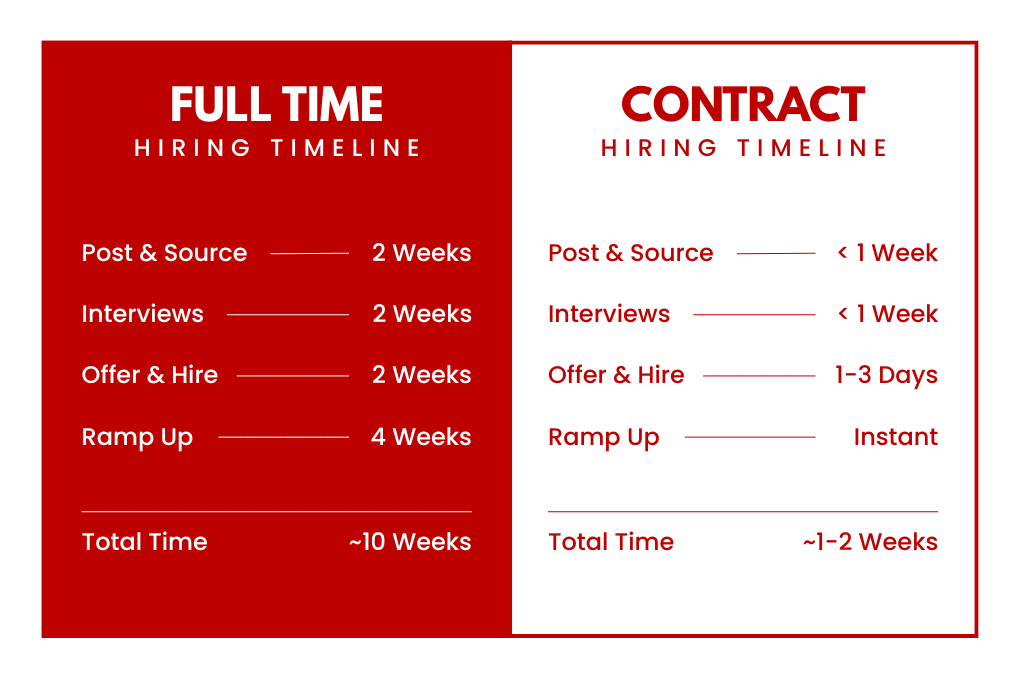

Here’s what hiring a compliance officer looks like: two weeks to post and source, three weeks to interview, two weeks for the offer and background check, then another month before they’re productive. That’s ten weeks minimum, and it assumes everything goes smoothly.

Now imagine you just got notice of a regulatory exam in eight weeks. Or your transaction monitoring system flagged 400 alerts last month instead of the usual 150. Or two business units just merged and someone needs to reconcile their completely different control frameworks.

You’re not hiring someone to join the team. You’re hiring someone to fix a specific problem before it becomes a regulatory finding.

That’s why banks hire the same contract auditors over and over. These people know what examiners look for because they used to be examiners. Or they’ve prepared so many banks for FDIC reviews that they can spot control gaps faster than your own audit team.

What Contract Auditors Actually Fix

Most contract auditors aren’t doing routine testing. They’re handling the reviews that nobody on staff has time for or the expertise to do well.

A community bank upgrading its core system might hire a contractor who’s done that exact implementation at five other banks. This person knows which controls break during migration, what data gets lost, and how to test whether everything actually works before you flip the switch. Your IT auditor probably doesn’t, because they’ve never done a core conversion before.

Same thing happens with specialized risks. If you need someone to review your Bank Secrecy Act program, you want someone who’s built BSA programs, not someone who read the regulation last month. The contractor might cost twice as much per hour as a full-time hire, but they’ll finish in half the time and catch twice as many issues.

Pre-exam work is where this really shows up. Banks hire contractors to run mock exams using the same testing methodology the OCC or Federal Reserve will use. Find the problems yourself, fix them quietly, and hope the real exam goes smoothly. It’s defensive, but it works.

The OCC’s Fall 2025 Semiannual Risk Perspective identifies credit, market, operational, and compliance risks as key themes facing banks, with cybersecurity threats from foreign state-sponsored actors and sophisticated cybercriminal groups targeting the financial sector among the most pressing operational concerns. Banks know this. So, they bring in people who’ve already helped other banks address those exact findings.

The Anti-Money Laundering (AML) Contractor You’ll Meet Everywhere

Every bank has met this person: the AML specialist who worked at three other regionals, knows every transaction monitoring vendor, and can write a Suspicious Activity Report in their sleep.

Banks hire them when alerts spike, when someone senior leaves suddenly, or when FinCEN changes its guidance and nobody on staff knows what it means yet. These contractors don’t need training on what structuring looks like or how to document a filing. They’ve already investigated a thousand cases.

Financial institutions filed 4.7 million suspicious activity reports in fiscal year 2024, according to FinCEN’s most recent year-in-review report released in June 2025. A decent chunk of those were probably written by contractors brought in to clear backlogs or handle complex investigations that would’ve taken permanent staff weeks to sort out.

This isn’t temp work. It’s specialized work that happens in bursts. Most banks don’t have enough AML alerts to keep three full-time investigators busy year-round. But during filing season or after a system upgrade, they might need five people for two months. Contract workers solve that mismatch.

Why the Math Works (Even Though It Looks Expensive)

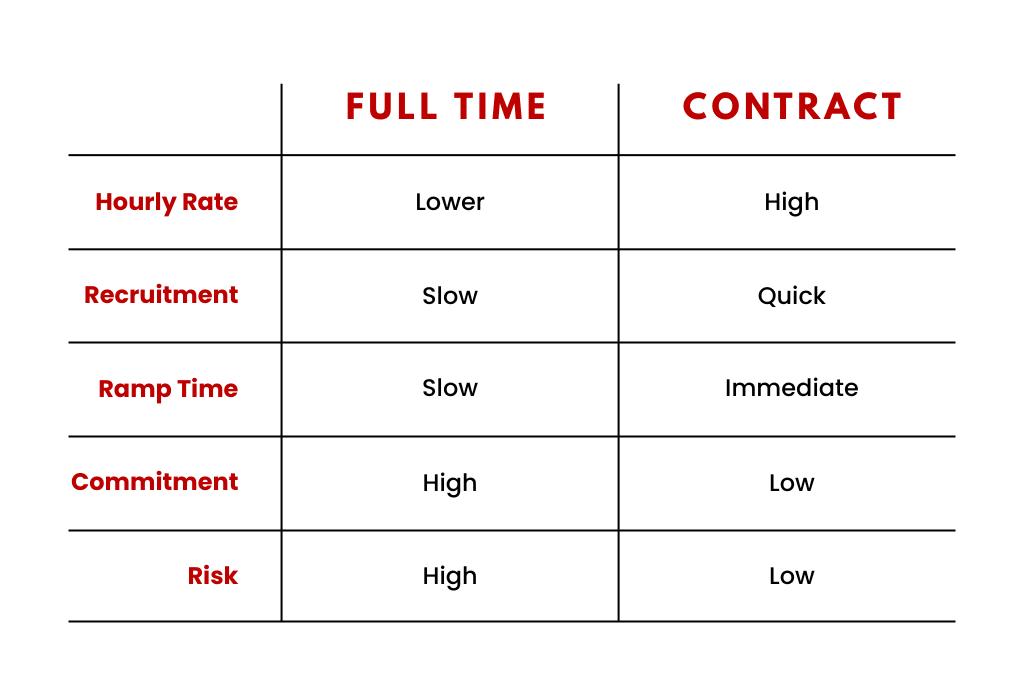

A contract compliance officer might bill $100 an hour. That’s $4,000 a week, $16,000 a month, roughly $96,000 for six months. A full-time hire at $85,000 a year costs less per hour once you add in benefits, but you’re committing to that salary indefinitely.

The real cost difference shows up in timing. If you hire full-time, you lose six weeks to recruiting and another month to onboarding. That’s ten weeks of paying someone who isn’t solving your problem yet. The contractor starts solving it on day three.

There’s also the risk calculation. The Consumer Financial Protection Bureau ordered over $750 million in penalties and consumer relief in 2024. One missed control weakness, one botched audit, one compliance gap that should’ve been caught: that can cost more than a decade of contractor bills.

Banks that staff too lean during exam cycles or merger integrations often pay for it later in remediation work, consent orders, and follow-up exams. Bringing in someone who’s done this before isn’t expensive insurance. It’s avoiding an unforced error.

What Separates the Contractors Worth Hiring

The best ones have pattern recognition you can’t teach.

They’ve reviewed enough loan files to spot underwriting drift before it becomes a systemic issue. They’ve seen enough transaction monitoring alerts to know which ones are actual money laundering and which ones are rich people doing rich people things. They’ve written enough exam responses to know what regulators want to hear versus what sounds good in a policy manual.

Credentials matter less than you’d think. A Certified Regulatory Compliance Manager (CRCM) or Certified Anti-Money Laundering Specialist (CAMS) designation proves someone passed a test. It doesn’t prove they can walk into your bank and deliver findings in three weeks.

What works better: ask for examples. Not general references, but specific projects. “Tell me about a time you found a BSA gap nobody else caught” gets you better information than “Can you send three references?”

The other thing good contractors do well is leave your team smarter than they found them. If someone fixes a compliance issue but nobody on staff understands how they fixed it, you’re just renting expertise. The contractors worth rehiring document everything, explain their reasoning, and make sure your people can handle it next time.

The Banks That Plan for This (Instead of Scrambling)

Some banks have stopped treating contract work as an emergency hire and started budgeting for it.

They know they’ll need extra auditors in Q2 for pre-exam work. They know their AML alerts spike every November. They know that every system upgrade needs someone who’s done that upgrade before. So, they plan for contractors the same way they plan for software licenses or audit fees.

This shift changes the caliber of people you get. Contractors who know they’ll be brought back for future projects invest more in understanding your bank. They build relationships with your staff. They’re not just parachuting in to collect a check.

Staffing firms have noticed this too. The banks that reach out six months in advance get better candidates than the ones calling with a two-week deadline. Planning also gives everyone time to clear background checks, complete compliance training, and actually start on time instead of losing a week to paperwork.

What’s Coming in 2026

Regulatory expectations keep expanding. The Office of the Comptroller of the Currency isn’t easing up on operational resilience, third-party risk, or fair lending supervision. If anything, they’re asking for more documentation, more testing, more proof that controls actually work.

Meanwhile, the talent pool for experienced compliance people keeps shrinking. Banks compete with consulting firms, fintech companies, and regulatory agencies for the same candidates. Contract work lets smaller banks access senior expertise they’d never be able to hire full-time.

Remote work has changed this too. A bank in Kentucky can now hire a BSA expert based in California without relocation costs or travel expenses. That expands the candidate pool and makes contract roles viable for banks that couldn’t attract that talent five years ago.

Why Some Banks Still Get This Wrong

Some banks don’t understand where to place their contract worker for them to be most effective. The worst use of a contractor: hiring a former examiner with 20 years of experience, then assigning them data entry work because “we need help catching up on documentation.”

That’s not a staffing strategy. That’s a waste.

The other mistake is treating contractors like outsiders. If you don’t give them access to the right data, the right people, or enough authority to make recommendations, they can’t do the work you hired them for. Then you complain that contractors don’t deliver value.

Some banks also balk at the hourly rate without thinking through the alternative. Yeah, paying someone $110 an hour feels wrong when you make $75 an hour. But if they solve a problem in four weeks that would’ve taken your team four months, it’s worth the cost.

What This Actually Means

Contract work in banking compliance isn’t a workaround for bad hiring. It’s how you staff for work that’s too urgent, too specialized, or too cyclical to handle with a permanent hire.

The banks that do this well treat contractors like the senior professionals they are. Clear objectives, real authority and access to decision-makers. The banks that struggle either underuse them or micromanage them until they’re useless.

Regulatory pressure isn’t decreasing. Compliance requirements aren’t getting simpler. And the talent market isn’t getting easier. Contract work is how banks manage that reality without pretending every role needs to be permanent or every project needs to wait for the perfect full-time hire.

You’ll keep hiring the same contractors because they keep solving the same problems faster than anyone else could.

Looking for a new employee to help with your banking compliance issues? Our team at PeopleSolutions is here to help! Reach out to one of our banking experts today to discuss the potential solutions we have to offer.

Alan Chamberlin

President, PeopleSolutions

(804) 404-2832

alanc@peoplesolutions.cc

Jon Burkhart

Division President, Banking, The Richmond Group USA

(804) 404-2819

jonb@richgroupusa.com