Federal contractors and subcontractors are taking on more work shaped by the CHIPS Act, the Infrastructure Investment and Jobs Act (IIJA), and Inflation Reduction Act (IRA) incentives at the same time that labor compliance has become harder to manage. CHIPS for America says the CHIPS Act provided $52.7 billion to support the domestic semiconductor industry, including $39 billion in semiconductor incentives and $11 billion in semiconductor R&D. DOE says IIJA-funded construction, alteration, or repair work must follow Davis-Bacon standards. The IRS says certain IRA clean energy incentives offer a significantly higher value when prevailing wage and apprenticeship requirements are met.

These requirements change what workforce risk looks like. Payroll accuracy, labor classification, fringe administration, subcontractor oversight, and apprenticeship tracking can now affect whether a contractor stays compliant, preserves credit value, avoids back-pay liability, and keeps the project moving. The Department of Labor says Wage and Hour Division enforcement recovered more than $259 million in back wages for nearly 177,000 employees in fiscal year 2025. This crackdown is a clear reminder that wage-and-hour mistakes still lead to real financial exposure.

Table of Contents

Why Workforce Compliance Risk Is Growing on CHIPS, IRA, and IIJA Projects

CHIPS, IRA, and IIJA Create Different Labor Obligations

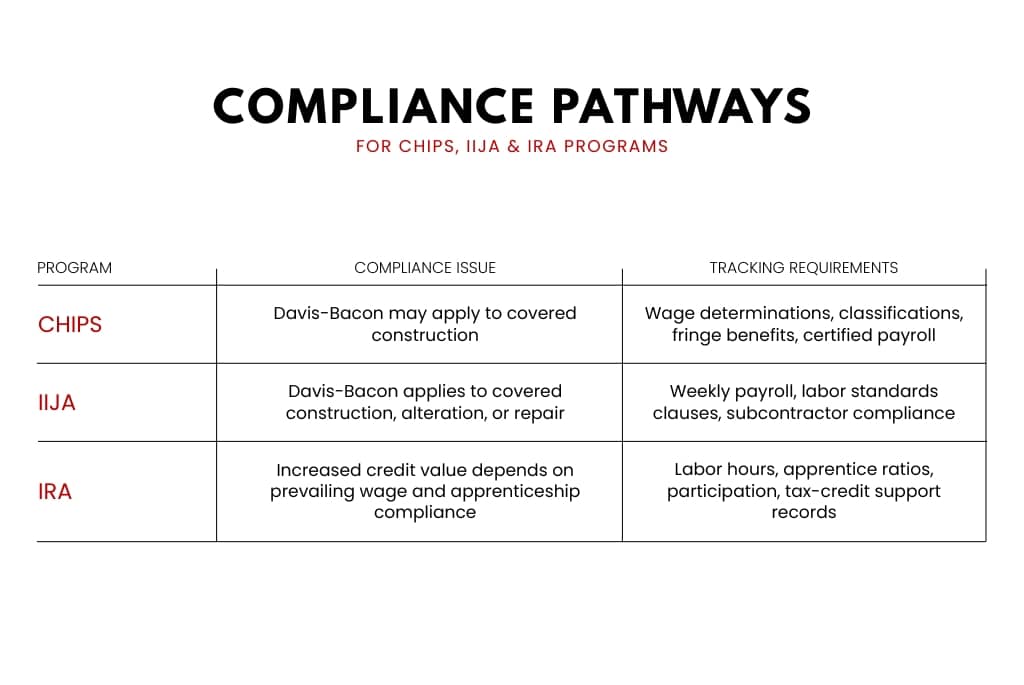

One of the most common mistakes on federally influenced projects is treating CHIPS, IIJA, and IRA requirements as if they all run through one labor-compliance system. They do not. CHIPS-funded construction projects and IIJA-funded construction, alteration, or repair work can trigger Davis-Bacon obligations. The IRA is different; it ties the increased value of certain credits and deductions to prevailing wage and registered apprenticeship compliance, which creates a separate tax-credit documentation track.

One project can involve more than one compliance pathway at the same time. A contractor may need to manage Davis-Bacon wage determinations, fringe obligations, weekly certified payroll, subcontractor flow-down requirements, and separate records strong enough to support an IRA bonus-credit claim. The risk here is that more projects now sit where multiple compliance systems overlap.

The Compliance Burden Now Hits Operations, Finance, and Tax at the Same Time

These issues do not stay in one department. A classification error can create underpayment exposure. A fringe shortfall can create compensation and reporting problems. A missed apprenticeship threshold can weaken the project’s tax-credit position. Under Davis-Bacon, the required wage includes both the base hourly rate and the required fringe benefits for the classification actually performed. Under the IRA, taxpayers seeking increased credit or deduction amounts generally need to satisfy both prevailing wage and apprenticeship requirements and keep records to support those claims.

Why This Matters More for Subcontractors and Multi-Employer Project Teams

The risk gets harder to control when labor is spread across multiple employers. DOL says covered subcontract agreements must include the required labor standards clauses and applicable wage determinations. That means subcontracting increases the number of points where classification, payroll setup, fringe treatment, and recordkeeping can drift. A prime contractor may not process every downstream payroll, but it still has a strong practical reason to care how those labor controls are being handled.

Where Federal Contractors Most Often Get Exposed

Payroll Errors That Trigger Scrutiny and Rework

At PeopleSolutions, we’ve seen firsthand how these requirements have been exposing federal contractors. One of the things we’ve seen recently is an increase in payroll errors triggering DOL scrutiny. Form WH-347 is available for the convenience of contractors and subcontractors submitting certified weekly payrolls on federal or federally assisted construction work. While the form itself is optional, the weekly certified payroll obligation is not.

That weekly cycle is what turns ordinary payroll mistakes into compliance problems. If the classification is wrong, the wage rate is wrong, overtime is inconsistent, or the certified payroll doesn’t match the underlying records, the contractor is not just fixing an internal pay error; they’re correcting a labor record they’ve already certified. The longer the issue stays in place, the more costly the correction becomes.

Misclassified Workers and Back-Pay Liability

When misclassification issues come up with these requirements, they’re trying to figure out whether the worker was paid under the correct Davis-Bacon classification for the work actually performed. DOL says laborers and mechanics on covered work must be paid the applicable prevailing wage, including fringe benefits, for the work they perform.

This is how back-pay liability builds. If a worker is placed in a lower-paid classification than the duties on site support, the underpayment can run across every affected hour already worked. Once that happens, the contractor may be dealing with retroactive wage corrections, fringe corrections, and corrected reporting.

Fringe Benefit Mistakes That Create Expensive Downstream Problems

Fringe benefit mistakes are often the quietest source of trouble. DOL’s fringe-benefit guidance makes it clear that the prevailing wage is the combination of the base hourly rate and the required fringe benefits for the applicable classification. A contractor can look at the wage line and think the payroll is correct while the total required compensation is still short.

Fringe errors can create more disruption than they seem to at first. Once the mistake has been repeated across workers and weeks, payroll has to be recalculated, certified payroll may need correction, and supporting records must be cleaned up. What started as a pay-structure mistake becomes a project-administration problem.

Missed Apprenticeship Ratios or Weak Records That Put IRA Credit Value at Risk

Another common issue PeopleSolutions is seeing is contractors missing the apprenticeship requirement or failing to keep the records needed to prove they met it. For IRA incentives that include apprenticeship rules, the IRS says the taxpayer generally has to satisfy three separate tests during construction: a labor-hours requirement, a ratio requirement, and a participation requirement. The labor-hours requirement is 15% for construction that begins in 2024 or later. The ratio requirement means the project has to follow the applicable apprentice-to-journeyworker ratio set by the registered apprenticeship program each day. The participation requirement means that if the taxpayer, contractor, or subcontractor employs 4 or more individuals at any time during construction, alteration, or repair, it must employ at least one qualified apprentice.

That’s where weak tracking becomes expensive. The final regulations say the taxpayer must maintain and preserve records sufficient to demonstrate compliance for each facility. At a minimum, that includes payroll records for each laborer and mechanic, including each qualified apprentice. For the apprenticeship side specifically, the IRS says records may include written requests for apprentices, agreements with registered apprenticeship programs, documents showing each program’s standards and required ratios, the project’s total labor hours and the hours worked by each qualified apprentice, daily apprentice-to-journey worker ratios, correspondence and denials tied to any good faith effort claim, and records of any failures, remediation steps, penalties, or complaints.

The financial downside is not minor. The IRS says taxpayers that satisfy prevailing wage and apprenticeship requirements can generally claim 5 times the base credit or deduction amount for covered incentives. On top of that, the IRS says a taxpayer that fails the apprenticeship requirement and wants to cure the failure generally must pay a penalty of $50 multiplied by the labor hours for which the requirement was not met, and that rises to $500 per labor hour if the IRS finds intentional disregard.

Why Payroll Accuracy Has Become a Strategic Capability

Payroll now affects project execution in a way many contractors still underestimate. DOE’s IIJA guidance highlights the weekly certified payroll requirement, and DOL notes that using the wrong wage determination can be disruptive and costly. Payroll accuracy now affects compliance, documentation quality, and how much cleanup a project team may have to absorb later.

Ensuring proper documentation and payroll accuracy now has the potential to save you a significant amount of money, but only when done right. If you don’t have the administrative capacity to keep up with these tasks, you risk penalties and potentially miss out on financial gains. Because of this, prime contractors are now looking for outside help like contract staffing agencies. Agencies like PeopleSolutions can manage payroll and compliance issues so that your team can focus on the actual work that needs done.

How Contract Staffing Helps Reduce Federal Workforce Compliance Risk

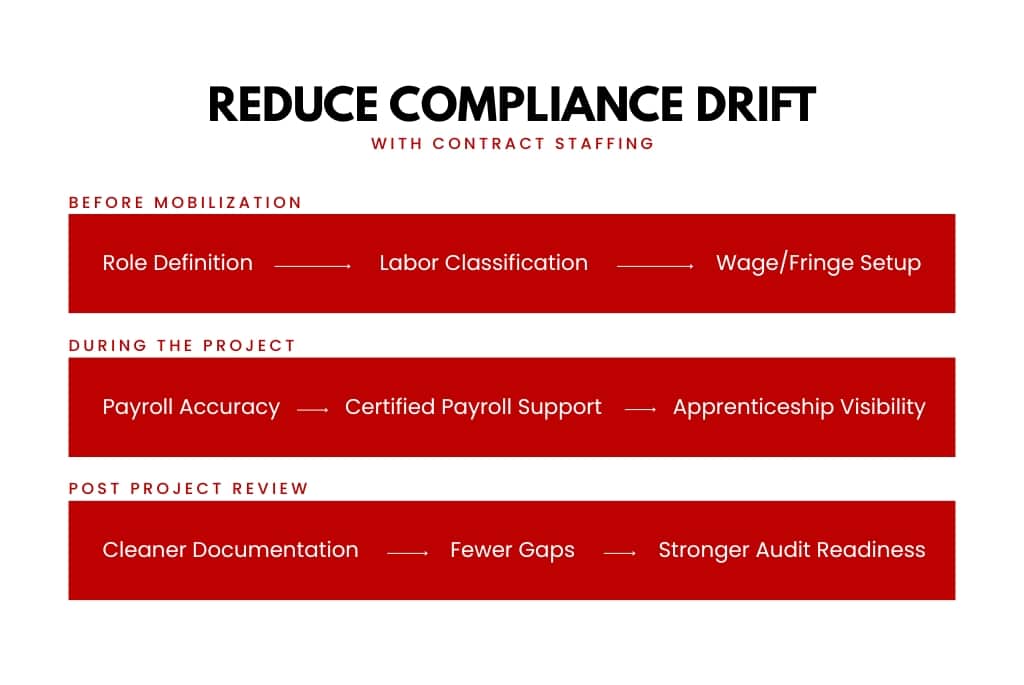

Contract staffing reduces more than a labor-availability problem when it’s structured correctly. On federally influenced projects, the value is labor classification, pay setup, and recordkeeping. Most costly compliance failures start here.

Better Labor Classification Before Mobilization

The first control point is classification. On covered work, the issue is whether the worker is mapped to the duties actually being performed on site. A stronger staffing process helps contractors define the role correctly before the worker starts instead of discovering later that the labor was paid under the wrong classification.

Cleaner Payroll Setup and Certified Payroll Support

A second control point is payroll setup. Contract staffing can reduce compliance risk when worker data, pay rates, and job assignments are set up consistently from the beginning. That creates a cleaner path from onboarding into payroll and from payroll into certified payroll reporting. On projects with weekly payroll obligations, small setup mistakes become more expensive every week they remain uncorrected.

Stronger Fringe Administration

Fringe obligations are one of the easiest places for a project to drift out of compliance. A contract staffing model can help by making sure the compensation structure is reviewed as a full prevailing wage obligation, not just a base-rate decision. That reduces the chance that hourly pay looks right while total required compensation is still short.

More Reliable Apprenticeship Tracking

On projects where IRA prevailing wage and apprenticeship requirements affect credit value, labor planning must support documentation. Contract staffing can help by giving contractors better visibility into workforce mix, apprentice utilization, and labor hours while the project is still in motion.

Fewer Documentation Gaps Across the Labor Model

The broader advantage is reduced fragmentation. The more labor decisions are split across disconnected internal teams, subcontractors, and outside vendors, the easier it is for classification, pay setup, fringe treatment, and apprenticeship records to fall out of sync. When you use a contract staffing service, the documentation and hiring process are connected and handled by a single team which leaves less room for errors.

PeopleSolutions is here to help federal contractors and subcontractors stay compliant, competitive, and audit-ready by improving labor classification, payroll control, apprenticeship tracking, and documentation discipline.

How PeopleSolutions Helps Federal Contractors Stay Compliant

PeopleSolutions fits best as a workforce-compliance partner inside a regulated project environment. We go beyond contract staffing by helping federal contractors and subcontractors manage labor classification, audit defense, apprenticeship tracking, and broader workforce compliance tied to CHIPS, IRA, and IIJA requirements.

Contractors often fail because the compliance process is fragmented. Payroll sits in one place, labor decisions sit in another, subcontractor oversight is inconsistent, and apprenticeship documentation is treated as a later problem. PeopleSolutions reduces that fragmentation and can lower risk in a way a generic recruiting vendor can’t.

If you’re looking for a partner who can help you navigate and mangage the compliance requirements for federal contractors, talk to the team at PeopleSolutions to see how we can best assist your team.

Frequently Asked Questions

What Is Form WH-347 Used For?

Form WH-347 is the commonly used weekly certified payroll form for covered Davis-Bacon and related construction work. DOL says the form is optional, but the weekly payroll submission requirement is still mandatory.

Does the IRA Use the Same Reporting Process as Davis-Bacon Certified Payroll?

No. WH-347 belongs to the certified-payroll side of Davis-Bacon compliance. The IRA uses a separate tax-credit compliance path, and the IRS says Form 7220 is used for certain prevailing wage and apprenticeship verification and correction reporting.

Can Subcontractors Create Davis-Bacon Compliance Risk for the Prime Contractor?

Yes. DOL says covered subcontract agreements must include the required labor standards clauses and applicable wage determinations, which is why downstream labor compliance matters so much.

Why Do Fringe Benefit Mistakes Cause So Many Problems?

Because prevailing wage compliance includes both the base hourly rate and the required fringe benefits. A contractor can think the wage rate is right while the total required compensation is still short.

How Can Contract Staffing Reduce Workforce Compliance Risk?

It can reduce risk when it improves worker classification before mobilization, standardizes payroll setup, reduces documentation gaps, supports cleaner certified-payroll records, and gives contractors better visibility into apprenticeship tracking.